Why High-Income Professionals Buy Franchises

Franchise ownership is defined as the purchase of a licensed right to operate a proven business model under an established brand, and it is the primary vehicle high-income professionals use to build wealth outside their W-2 income. Executives, directors, and senior managers earning $150,000–$500,000 annually face a structural problem: their wages are taxed at the highest marginal rates, and their investment options rarely generate the tax offsets that business ownership does. Franchising solves both problems at once. It delivers a tested operational system that reduces execution risk, and it opens access to deductions including Section 179 depreciation and the Qualified Business Income (QBI) deduction that wage earners simply cannot access. That combination is why high-income professionals buy franchises at a rate that continues to outpace general entrepreneurship.

Why high-income professionals buy franchises instead of starting businesses

The core reason high earners choose franchises over startups is execution risk. A startup requires proving product-market fit, building brand recognition, and developing operational systems from scratch. A franchise eliminates all three. Franchising is execution-risk investing: the product-market fit is already proven, and success depends entirely on the franchisee's ability to operate the system effectively. That is a fundamentally different risk profile, and it favors professionals who have spent careers managing teams and executing within structured environments.

The survival data supports this. Franchises report survival rates as high as 90% in certain service sectors, a figure that independent startups rarely approach. That gap exists because franchises carry collective buying power, pre-negotiated supplier contracts, and national marketing infrastructure. A single-unit operator benefits from cost structures that an independent business owner would need years and significant capital to replicate.

Pro Tip: Before evaluating any franchise, request the Franchise Disclosure Document (FDD) and review Item 19, the Financial Performance Representation. This is the only legally compliant source of actual unit-level revenue and profit data.

The risk reduction also extends to brand trust. Customers already recognize the name, which shortens the customer acquisition cycle. For a professional accustomed to managing risk in corporate settings, that brand equity functions like a built-in moat. Reviewing the risks of franchise investment before committing capital remains the right first step, but the baseline risk profile is structurally lower than a cold startup.

What tax advantages do high-income franchise owners gain?

The tax case for franchise ownership is the most compelling argument for W-2 earners in the $300,000–$500,000 income range. Dual-income households earning $400,000+ can reduce their effective tax rate significantly using franchise deductions including Section 179 depreciation and the QBI deduction, provided they meet IRS participation rules. These are not loopholes. They are standard tax code provisions that business owners access and wage earners cannot.

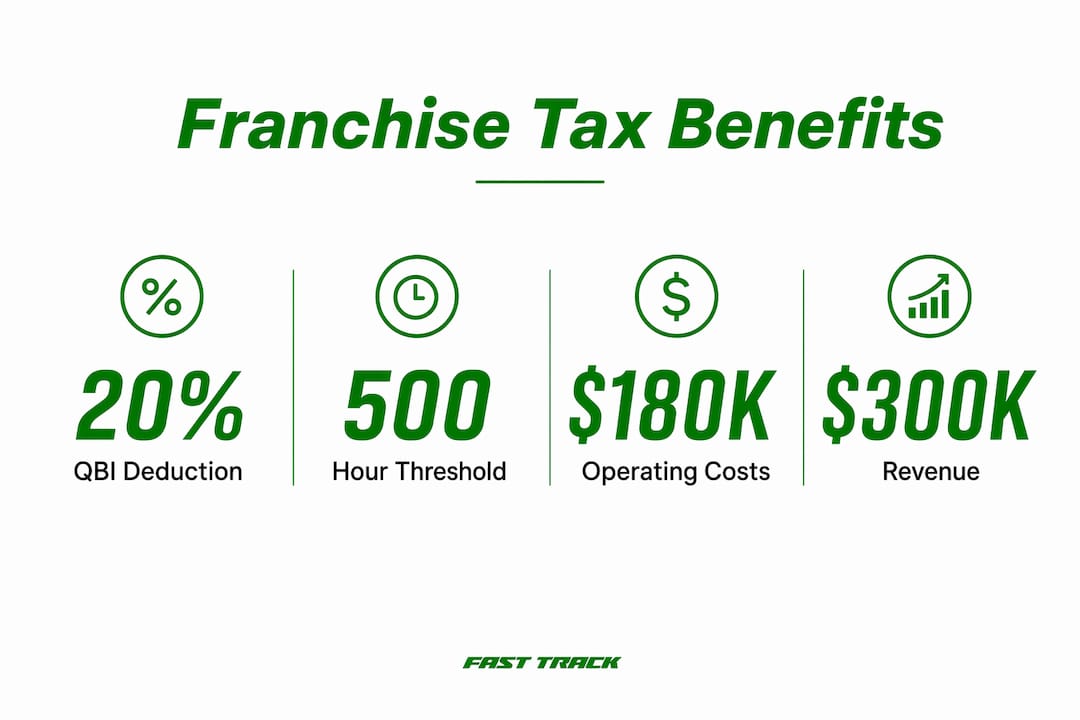

The mechanics work like this. A small service franchise generating $300,000 revenue with $180,000 in operating costs produces $120,000 in profit. Against that profit, the owner can apply the QBI deduction (up to 20% of qualified business income), Section 179 equipment write-offs, and contributions to a Solo 401(k) that exceed standard W-2 retirement limits. The net taxable income from the franchise drops substantially, and those deductions offset income that would otherwise be taxed at the top marginal rate.

| Tax Tool | W-2 Wage Earner | Active Franchise Owner |

|---|---|---|

| QBI Deduction | Not available | Up to 20% of qualified income |

| Section 179 Depreciation | Not available | Full equipment cost in year one |

| Solo 401(k) Contributions | Limited to employer plan | Up to $69,000 annually (2024 limit) |

| Business Expense Deductions | Severely restricted | Full operating costs deductible |

The critical variable is IRS material participation. The IRS applies a 500-hour annual threshold as the primary test for active participation. Owners who fall below that threshold have their franchise losses reclassified as passive, which means those losses cannot offset W-2 income. The tax benefit disappears entirely. This is the most misunderstood rule in franchise tax planning, and it is the reason that working with a qualified tax strategist is not optional. A firm like The Tax Refinery specializes in exactly this kind of high-income business tax planning and can model the real numbers before you commit.

Pro Tip: Track your participation hours from day one using a simple time log. The IRS can audit material participation claims up to three years back, and documentation is your only defense.

How do high-income professionals leverage multi-unit and territory ownership?

Single-unit ownership is the entry point. Territory rights and multi-unit development agreements are where high-income earners build real wealth. High-income earners favor territory rights over individual units because they generate royalties and multi-unit fees through oversight rather than direct labor. A territory owner conducts strategic reviews weekly or monthly rather than working 40–60 hour weeks on the floor. That model aligns with how executives already operate.

The types of franchise ownership models available to high earners include:

- Single-unit operator: Owns and manages one location. Highest time commitment, lowest capital requirement.

- Multi-unit developer: Signs an agreement to open multiple units over a set timeline. Requires hiring district managers and building a management layer.

- Area representative or territory owner: Recruits and supports franchisees within a defined geography. Income comes from royalty splits and initial franchise fees.

- Master franchisee: Holds sub-franchising rights for a region or country. Highest capital requirement, highest income ceiling.

Scaling beyond 10–15 units requires a full management hierarchy with district and regional managers. At that scale, the owner functions as an investor-leader rather than an operator. The income model shifts from direct profit to management fees, royalty overrides, and equity appreciation across the portfolio. Sectors that fit this model well include home services, wellness, and business-to-business services, where recurring revenue and low physical inventory make multi-unit management tractable.

What operational commitments should high-income professionals expect?

The most common mistake high-income franchise buyers make is underestimating the work required in the first 12–18 months. Many professionals underestimate the initial workload in franchise ownership, particularly during ramp-up when staff training and operational stabilization demand intensive owner involvement. The advertised "semi-absentee" model is a post-stabilization reality, not a launch-day reality.

Realistic expectations for the ramp-up phase include:

- Months 1–6: Owner involvement of 20–40 hours per week to train staff, establish vendor relationships, and hit the IRS material participation threshold.

- Months 6–18: Gradual transition to a general manager model as operations stabilize and a competent management team is in place.

- Year 2 onward: Oversight role of 5–15 hours per week if the right manager is hired and retained.

The quality of the general manager is the single biggest variable in this transition. Entry-level or low-wage supervisors often fail, leading to stalled revenue and, critically, IRS scrutiny on passive loss classification. Paying a market-rate general manager is not an optional cost. It is the mechanism that protects both the business and the tax strategy.

Pro Tip: Budget your general manager salary into your pro forma before you sign the franchise agreement. If the unit economics do not work with a $60,000–$80,000 manager salary included, the franchise is not viable for a semi-absentee model.

Understanding how franchise profitability is calculated before signing any agreement gives professionals a clear picture of whether the numbers support the staffing model they intend to run.

Key Takeaways

High-income professionals buy franchises because the combination of proven systems, tax advantages, and scalable ownership models produces wealth-building outcomes that W-2 income alone cannot replicate.

| Point | Details |

|---|---|

| Execution risk is lower | Franchises offer proven systems and brand recognition, reducing the risk that kills most startups. |

| Tax benefits require active participation | QBI deductions and Section 179 write-offs only apply when the IRS material participation test is met. |

| Territory rights scale income efficiently | Area representative and multi-unit models generate income through oversight, not direct labor. |

| Ramp-up demands real work | The first 12–18 months require significant owner involvement before a semi-absentee model becomes viable. |

| Manager quality determines success | Hiring an experienced general manager protects both profitability and the franchise's tax classification. |

The part most franchise buyers get wrong

Franchising rewards execution discipline, not entrepreneurial ambition. I have seen this pattern repeatedly: the professionals who struggle most in franchise ownership are the ones who bought the concept of passive income. The ones who succeed treated it like a business from day one, staffed it properly, and tracked their hours.

The tax benefits are real. The survival rates are real. But neither materializes without active management in the early stages. Veterans and professionals with structured management backgrounds consistently outperform casual buyers in franchise performance, and the reason is not capital. It is operational discipline applied consistently from the first week of operation.

The other thing I would push back on is the idea that franchise ownership is a side project. For the first year, it is a second job. After that, with the right team, it becomes a wealth-building asset that runs largely without you. The professionals who accept that trade-off upfront are the ones who build multi-unit portfolios. The ones who resist it sell their unit at a loss within two years.

If you are a high earner evaluating franchise ownership as a path to financial independence, the question is not whether the model works. It does. The question is whether you are willing to do the work required to get it to the point where it works without you.

— Cody

How Franchise Fast Track connects high-income buyers with the right opportunities

Finding the right franchise opportunity as a high-income professional is not a search problem. It is a qualification and matching problem. Most franchise lead generation channels are built for volume, not for buyers who earn $150,000–$500,000 annually and need a model that fits their tax situation, time constraints, and income goals.

Franchise Fast Track is built specifically for this gap. The platform delivers verified appointments with high-income professionals, executives, directors, and senior managers who are actively evaluating franchise ownership. Franchisors using Franchise Fast Track report a lead-to-close rate of 34%, which reflects the quality of buyer the system attracts. If you are a franchisor looking to reach qualified, funded buyers, or a professional ready to explore ownership with expert support, Franchise Fast Track is where that conversation starts.

FAQ

Why do high-income earners prefer franchise models over startups?

Franchises eliminate the need to prove product-market fit and build brand recognition from scratch. The proven operational system reduces execution risk, which is the primary concern for professionals managing significant capital.

What is the QBI deduction and how does it apply to franchise owners?

The Qualified Business Income deduction allows eligible franchise owners to deduct up to 20% of qualified business income from taxable income. It is not available to W-2 wage earners, making it one of the most significant tax advantages of franchise ownership.

How many hours must a franchise owner work to qualify for tax deductions?

The IRS material participation test requires at least 500 hours of annual involvement as the primary threshold. Owners who fall below this level risk having their franchise losses reclassified as passive, which eliminates deductions against W-2 income.

What is a territory rights model in franchising?

A territory rights or area representative model gives the owner the right to recruit and support franchisees within a defined geography. Income comes from royalty splits and initial franchise fees rather than direct unit operations.

When can a franchise owner shift to a semi-absentee model?

Most franchise owners can transition to a semi-absentee role after 12–18 months, once operations are stable and a qualified general manager is in place. Attempting this transition too early is the most common cause of early-stage franchise failure.

Recommended

- Franchise Fast Track - The Only System Built To Deliver High-Income Franchise Buyers.

- How to Advertise a Franchise to Capital-Ready Candidates | Franchise Fast Track Blog

- Franchise Ownership for Executives: A Strategic Guide | Franchise Fast Track Blog

- Franchising Pros and Cons: A 2026 Guide for Franchisors | Franchise Fast Track Blog

Ready to see results like these for your franchise?

Stop wasting money on leads that never close. Start getting hundreds of replies from high-net-worth professionals daily.