How to Evaluate a Franchise Investment Opportunity

Evaluating a franchise investment opportunity is the process of systematically reviewing a franchisor's financial disclosures, system health, and legal terms to determine whether the business can generate sustainable returns for your specific goals. The industry term for this process is franchise due diligence, and it typically spans 60–90 days before you sign any agreement. Done correctly, it protects you from buying into a declining system, overestimating income, or underestimating startup costs. Done poorly, it costs you six figures and years of your life.

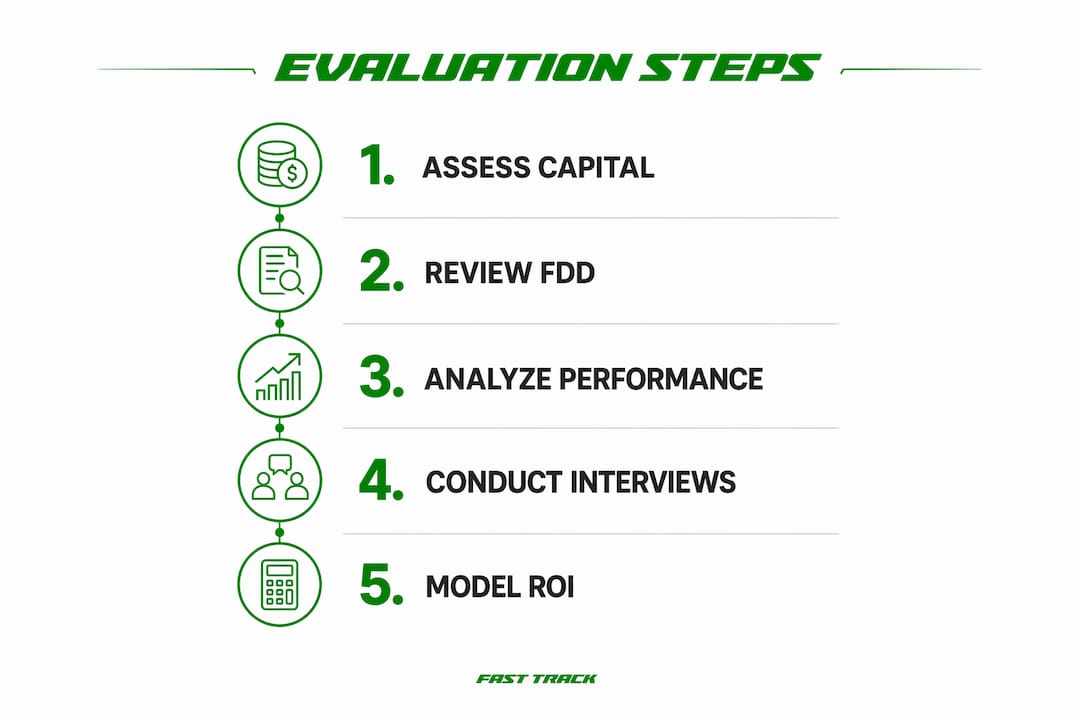

How to evaluate franchise investment opportunity readiness before you shop

The biggest mistake investors make is shopping for franchises before they know what they can actually afford. Start with a clear picture of your liquid capital, your risk tolerance, and your income needs. These three factors determine which franchise categories are even worth your time.

Define your capital and working capital reserves

Most franchise opportunities require an initial investment between $100,000 and $500,000 or more. That number covers the franchise fee, buildout, equipment, and initial inventory. What it often does not cover is the cash you need to survive the ramp-up period.

Professional franchise accountants recommend setting aside 3–6 months of operating expenses, typically $80,000–$150,000, as working capital beyond what the FDD lists. Franchisors have a legal incentive to show the minimum required investment, not the realistic one. Budget conservatively.

Clarify your income expectations and time commitment

Set a specific monthly income target before you evaluate any franchise. Then model whether the franchise can realistically hit that number within 18–24 months, which is the average payback period for most franchise investments. If the math does not work at the median revenue figure, move on.

Your time commitment matters just as much as your capital. Owner-operator models demand 50–60 hours per week in year one. Semi-absentee models require less time but typically cost more upfront. Know which model fits your life before you fall in love with a brand.

- Determine your total liquid capital available for investment

- Set a minimum monthly income target and a timeline to reach it

- Decide between owner-operator and semi-absentee models

- Identify your maximum risk tolerance as a percentage of net worth

- Confirm all financial partners are aligned before proceeding

Pro Tip: Marital or partnership conflicts rank among the top causes of franchise business failures. Every financial partner must review the numbers and agree before you sign anything.

What does the FDD reveal about a franchise's true health?

The Franchise Disclosure Document is the single most important document in franchise opportunity evaluation. The FTC requires franchisors to provide it at least 14 days before you sign any agreement or pay any money. Use every one of those days.

The FDD contains 23 items. Three of them carry the most weight for any serious investor.

Item 7: total estimated investment

Item 7 lists every cost required to open and operate the franchise through the initial period. Read it as a floor, not a ceiling. Compare the FDD figures against what current franchisees actually spent. The gap between the two numbers tells you how accurate the franchisor's projections are.

Item 19: financial performance representations

Item 19 is where franchisors voluntarily disclose revenue and earnings data. Not all franchisors include it, and that absence is itself a red flag. Reject any franchise that provides no Item 19 data. When data is present, use the median and 25th percentile figures for your financial model, not the average. Averages are skewed by the top 10% of performers and will make the opportunity look better than it is for most buyers.

Item 20: unit openings and closures

Item 20 tracks how many units opened, closed, or transferred over the past three years. A declining unit count over three consecutive years is the clearest red flag in the entire document. It signals that franchisees are leaving faster than new ones are joining, regardless of what the marketing materials say.

| FDD Item | What to look for | Red flag |

|---|---|---|

| Item 7 | Total startup cost range | Gap between FDD estimate and actual franchisee spend |

| Item 19 | Median and 25th percentile revenue | No disclosure or data showing only top performers |

| Item 20 | Net unit growth over 3 years | Net unit loss in any 2 of the last 3 years |

Pro Tip: Hire a franchise disclosure specialist to review the FDD before you sign. A $3,000 legal review is cheap compared to a $300,000 mistake.

How do you validate a franchise through franchisee interviews?

Franchisee validation calls are the most underused tool in franchise investment analysis. The FDD lists current franchisee contact information in Item 20. Use it. Then go further.

Contact 10–15 current franchisees and 3–5 former franchisees for a complete picture. Former franchisees give you the honest story about exit hurdles, profitability ceilings, and franchisor support failures that current owners may be reluctant to share. Do not limit yourself to the contacts the franchisor recommends.

Ask these questions on every validation call:

- What was your actual investment compared to the FDD estimate?

- How long did it take to reach break-even?

- How responsive is the franchisor's support team when you have a problem?

- What do you know now that you wish you had known before signing?

- Would you buy this franchise again at the same price?

The answers to questions four and five are the most revealing. Consistent negative answers across multiple franchisees signal a systemic problem, not individual bad luck.

For objective third-party data, check the SBA 7(a) loan default rate for the franchise brand. Default rates under 5% indicate that most franchisees generate enough cash flow to service their debt. A high default rate means franchisees are struggling financially, regardless of what the franchisor's marketing claims.

"The most valuable validation calls are the ones the franchisor did not give you the number for." This is where the real picture of franchisee satisfaction and profitability emerges.

What financial benchmarks separate a good franchise from a bad one?

Franchise profitability assessment requires specific benchmarks, not gut feelings. Healthy franchise systems deliver a cash-on-cash return of 18–35% in year two, maintain EBITDA margins between 12–22%, and keep total fees below 10% of gross revenue.

Cash-on-cash return measures your annual pre-tax cash flow divided by your total cash invested. A 20% return on a $200,000 investment means $40,000 in annual pre-tax cash flow. That is the minimum acceptable threshold for most investors taking on the risk and labor of franchise ownership.

Fee burden and closure rate thresholds

Total fees, including royalties and advertising fund contributions, above 11% of gross revenue are a warning sign. High fee burdens compress margins and make it harder to reach profitability, especially in low-margin service categories. Check the royalty rate in Item 6 and the advertising fund rate in Item 11 of the FDD.

Annual closure rates above 5% indicate a system under stress. Cross-reference the closure rate from Item 20 against the SBA default data for a complete picture of franchise system health.

Modeling ROI over the full franchise term

A complete franchise investment analysis includes the exit. Most franchise agreements run 10 years. At exit, resale multiples of 2–4 times seller's discretionary earnings are typical for healthy systems. Model your internal rate of return across the full term, including SBA loan payoffs, transfer fees, and the resale value. A franchise that looks marginal on annual cash flow can still be a strong investment if the exit multiple is high.

Pro Tip: Use a franchise bookkeeping framework to track EBITDA and cash-on-cash return from day one. Investors who measure these metrics monthly catch problems early and protect their investment.

| Metric | Healthy benchmark | Red flag threshold |

|---|---|---|

| Cash-on-cash return (year 2) | 18–35% | Below 15% |

| EBITDA margin | 12–22% | Below 10% |

| Total fees (royalty + ad fund) | Under 10% of gross revenue | Above 11% |

| Annual closure rate | Under 5% | Above 5% |

| SBA 7(a) default rate | Under 5% | Above 7% |

Key Takeaways

Rigorous franchise due diligence, anchored in FDD analysis, franchisee validation, and financial benchmarking, is the only reliable way to assess franchise potential and protect your investment.

| Point | Details |

|---|---|

| Start with self-assessment | Define your capital, income target, and risk tolerance before evaluating any franchise. |

| Prioritize FDD Items 7, 19, and 20 | These three items reveal true startup costs, realistic earnings, and system health. |

| Conduct 10–15 validation calls | Include 3–5 former franchisees to get honest feedback the franchisor cannot filter. |

| Apply financial benchmarks | Target 18–35% cash-on-cash return in year two and total fees under 10% of gross revenue. |

| Model the full investment term | Include resale multiples and SBA loan payoffs to calculate your true internal rate of return. |

The evaluation mistakes I see serious investors make

Most investors I work with are sharp, financially literate people. They read the FDD. They run the numbers. And then they still make the same mistake: they fall in love with the brand before the math confirms it deserves their attention.

Brand recognition feels like safety. It is not. A recognizable name does not guarantee franchisee profitability. The FDD does not lie, but it does require you to read it skeptically. The franchises that look best in the marketing materials are often the ones with the most aggressive fee structures.

The second mistake is underestimating the ramp-up period emotionally and financially. Most investors model break-even at 12 months because that is the optimistic scenario. The realistic scenario is 18–24 months. If you cannot sustain yourself financially and psychologically for two years without hitting your income target, you are not ready to buy that franchise yet.

The third mistake is skipping professional review to save money. A franchise attorney's review costs roughly $3,000. A bad non-compete clause or a mandatory arbitration provision can cost you far more than that if the relationship with the franchisor sours. Hire the lawyer. Hire a franchise-specific accountant. These are not optional expenses for serious investors.

The investors who succeed treat franchise evaluation like a financial analyst treats a stock. They use weighted scorecards that assign points to financial performance, system health, investment cost, and support quality. They compare three to five franchises side by side before committing. Emotion is a terrible co-investor.

— Cody

Franchise Fast Track connects you with vetted franchise opportunities

Serious franchise buyers need more than a checklist. They need access to verified opportunities, real franchisee contacts, and the tools to run a disciplined evaluation from start to finish.

Franchise Fast Track is built specifically for high-income investors who want to move through the evaluation process without wasting time on unqualified opportunities. The platform connects executives, directors, and senior managers with vetted franchise systems and provides the resources needed to assess franchise potential at a professional level. From FDD analysis tools to qualified franchise leads, Franchise Fast Track gives serious buyers the infrastructure to make confident, data-driven decisions. If you are ready to invest with discipline, start your evaluation with the tools built for buyers who take this seriously.

FAQ

What is the minimum due diligence period before signing a franchise agreement?

The standard due diligence process spans 60–90 days, and the FTC requires franchisors to provide the FDD at least 14 days before you sign any agreement or pay any fees.

Which FDD items matter most for franchise investment analysis?

Items 7, 19, and 20 are the most critical. They reveal total startup costs, financial performance data, and the system's unit growth or decline over the past three years.

How many franchisee validation calls should I make?

Contact 10–15 current franchisees and 3–5 former franchisees. Former owners provide the most candid feedback about profitability and franchisor support.

What cash-on-cash return should I expect from a healthy franchise?

Healthy franchise systems deliver a cash-on-cash return of 18–35% in year two. Returns below 15% in year two indicate the investment may not justify the risk and labor involved.

How do I use SBA loan data to assess franchise risk?

Franchise brands with SBA 7(a) loan default rates under 5% show that most franchisees generate sufficient cash flow to cover their debt obligations. Rates above 7% are a serious warning sign.

Recommended

- Risks of Franchise Investment: 2026 Investor Guide | Franchise Fast Track Blog

- How Do You Open a Franchise | Franchise Fast Track Blog

- How Do I Become a Franchise Owner: A Franchisor's Roadmap | Franchise Fast Track Blog

- How to Become a Franchise Owner: Your Essential Guide | Franchise Fast Track Blog

Ready to see results like these for your franchise?

Stop wasting money on leads that never close. Start getting hundreds of replies from high-net-worth professionals daily.